Don't Diss Direct Mail

It's easy to overlook the value of a mailed direct marketing campaign in a world of emails and TikTok. However, it's more valuable than ever. Here are some reasons why.

Higher Response Rates. Direct mail has always been a leader in response rates, logging around 9% for established clients and 5% for prospects. Also, almost 50% of people over 45 will open envelopes or read postcards. Ever since remote work became popular, these workers wait for the daily "mail moment" as USPS calls it.

Plenty of Personalization Options. Consumers love these, and you can add your QR code to make it easier for them to join, like and follow you online.

Build Trust. Consumers tend to trust printed messaging over online messaging as it's impossible to infect a client's computer with malware by sending them a postcard. Direct mail is especially popular with the less computer-savvy.

Zero In. First-time buyers who are still renting need different messages than homeowners. So do different age groups—you don't want to talk to Gen Zers and Millennials the same way. Direct mail makes it easy to define and target each group in your database.

You Already Have a Direct Marketing Partner. I have access to technology that makes it easy for us to prepare and deliver professionally designed direct mail campaigns. Contact me and I'll introduce you to products like Every Door Direct Mail (EDDM), a USPS service that empowers you to reach prospects across an entire ZIP code.1

Why Some Sellers Insist on Silly Prices

Most of your seller clients will agree on a listing price for their home after you explain the strategy behind your calculations. But a few aren't great at taking advice and will insist that you list their home for way too much, even if the price scares potential buyers away. Even worse, they always have a reason why they shouldn't budge on price. Here are a few of those reasons (get ready to roll your eyes).

My neighbor agrees with my price. You can substitute plenty of words for neighbor here, but it doesn't change the fact that the price is too high. Sellers often don't realize that people will agree with their price simply to be supportive—something you may have to explain.

Prices are only going to go up. While home values do rise over time, that takes longer than it takes to sell a house. Unless your seller is happy holding on to their house for months or years, it doesn't make sense to overprice it.

I want some wiggle room when we negotiate. This sounds clever to the seller, but it tends to backfire. The higher the price, the more you'll end up haggling. This is because the longer the house is on the market, the more buyers' agents will come in with a lower offer.

The right buyer won't mind paying. If a seller insists they're waiting for the right buyer, chances are they've already encouraged those right buyers to pass on their house and buy another that's priced fairly. Remind your seller that buyers and agents are armed with market data and won't be fooled by an unreasonably high price.

Buyers' agents aren't doing their job. Agents show buyers several houses if possible. This enables their client to compare their features, locations...and prices. Buyer's agents aren't trying to find fault with the seller's home. Instead, they feel it's their responsibility to tell their client that the house isn't competitively priced, especially when compared to properties with similar features.2

Real Estate-Related Myths That Won't Die

You're already familiar with the 20% down payment myth which is still going strong.

Over 60% of respondents to a recent real estate survey think it's mandatory, and over 20% think they'll need to put down even more money down. But here are some others to keep in mind.

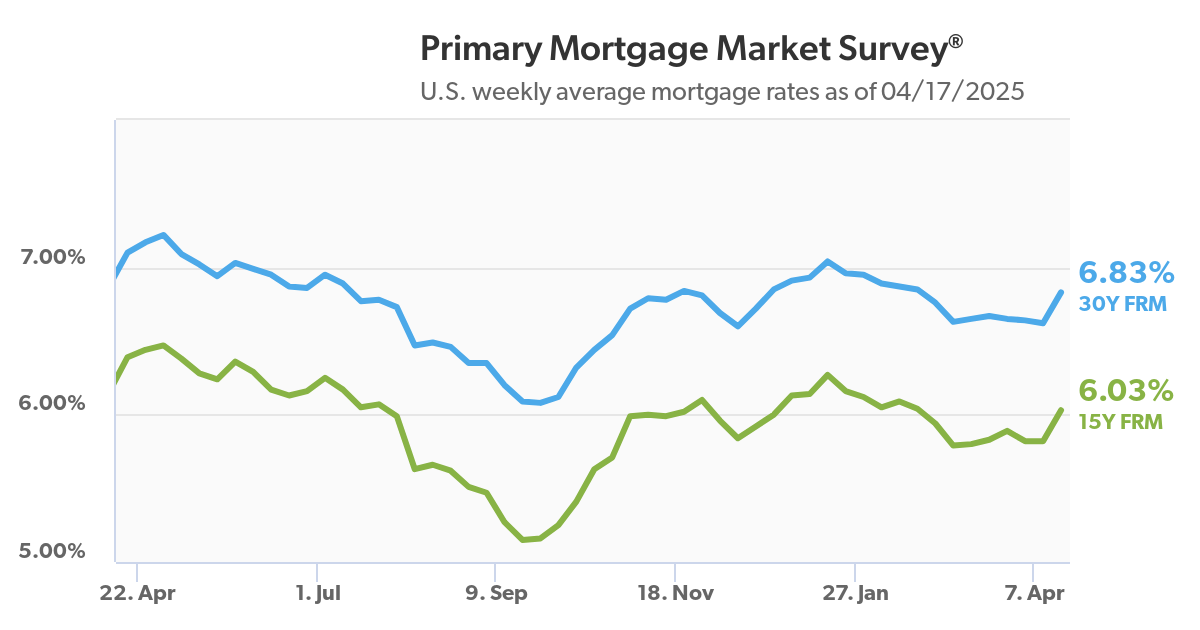

- Just 12% of respondents knew that the current rate for a 30-year mortgage is hovering around 7.5% - 8%. Around 25% of respondents were way off track, saying that it was over 10%. (The last time rates reached 10% was more than 30 years ago in 1990.)

- While homeowners spend just over $13,000 annually on utilities, maintenance, and improvements, 48% of Americans believe these homeowner expenses cost less.

- 23% of non-homeowners think saving for a down payment will be the most challenging part of buying a home, but only 8% of homeowners say it actually is.

- The average first-time home buyer is 36, but 73% of Americans think it's much younger.

- While 73% of Americans don't think homes are affordable now, 60% underestimate the median home price. Just 14% got this right.

- You know it's your responsibility to communicate with sellers and agents, but 65% of non-homeowners think it's the buyer's responsibility to contact the seller. This last myth probably contributes to why some buyers think they'll save money without an agent.

Homeowners' Insurance Premiums Keep Rising

Even though Southwest Florida has been hit by two major hurricanes in less than a year, the area is still a hot destination for sun-seeking homeowners. Insurance companies aren't taking such an optimistic view, as homeowners' premiums in Cape Coral and nearby cities are soaring.

Insurance companies, stung by recent natural disasters, are trying to claw back their losses by hiking rates or refusing to insure homes in areas they consider disaster-prone. For example, many Florida homeowners' premiums have tripled in just five years, according to the industry group Insurance Information Institute.

Flood insurance premiums are rising in vulnerable areas as well. The federal National Flood Insurance Program recently changed their pricing algorithm to tie premiums to risk. This increased insurance prices for waterfront ZIP codes, with average premiums now more than double earlier prices.

While some would-be buyers are balking at rising insurance premiums, it hasn't stopped many buyers from heading to disaster-prone areas. Some Florida and California counties have seen a big post-pandemic rise in populations, although around 30% of builders in these states claim they're seeing a slowdown in sales.

Even big spenders can get jittery about insurance costs. One California agent described a home for sale within Los Angeles' affluent Pacific Palisades neighborhood that was priced at $13.5 million. Interested buyers walked away after receiving insurance estimates from $100,000 to $300,000 per year.4

Honey, I Shrunk the House: Why Builders Are Downsizing

A combination of higher mortgage rates and other costs has resulted in builders reducing their floor plans' square footage. Some are opting for smaller living rooms and fewer bedrooms. Buyers also like multi-function features, including kitchen islands with drawers and drop-leaf dining tables.

Construction of homes with fewer than three bedrooms increased 9.5% in 2022 year-over-year, with construction of attached multi-story homes with fewer bedrooms rising by 37% compared to 2019. Detached homes increased 11% over the same time period.

Construction of homes with fewer than three bedrooms increased 9.5% in 2022 year-over-year, with construction of attached multi-story homes with fewer bedrooms rising by 37% compared to 2019. Detached homes increased 11% over the same time period.

Builders aren't simply downsizing the entire floorplan; instead, they're increasing the size of multi-use rooms like kitchens and living or "great" rooms to accommodate the preferences of buyers with hybrid or 100% remote work schedules.

"People are essentially changing the layout of their homes to reflect the fact that it's more expensive to get a 30-year fixed mortgage and people are typically working two days a week out of their homes," said Timothy Savage, a clinical assistant professor at NYU's Schack Institute of Real Estate.5

Sources: 1designdistributors.com, 2lightersideofrealestate.com, 3realestatewitch.com, 4programbusiness.com, 5axios.com

Recent Comments