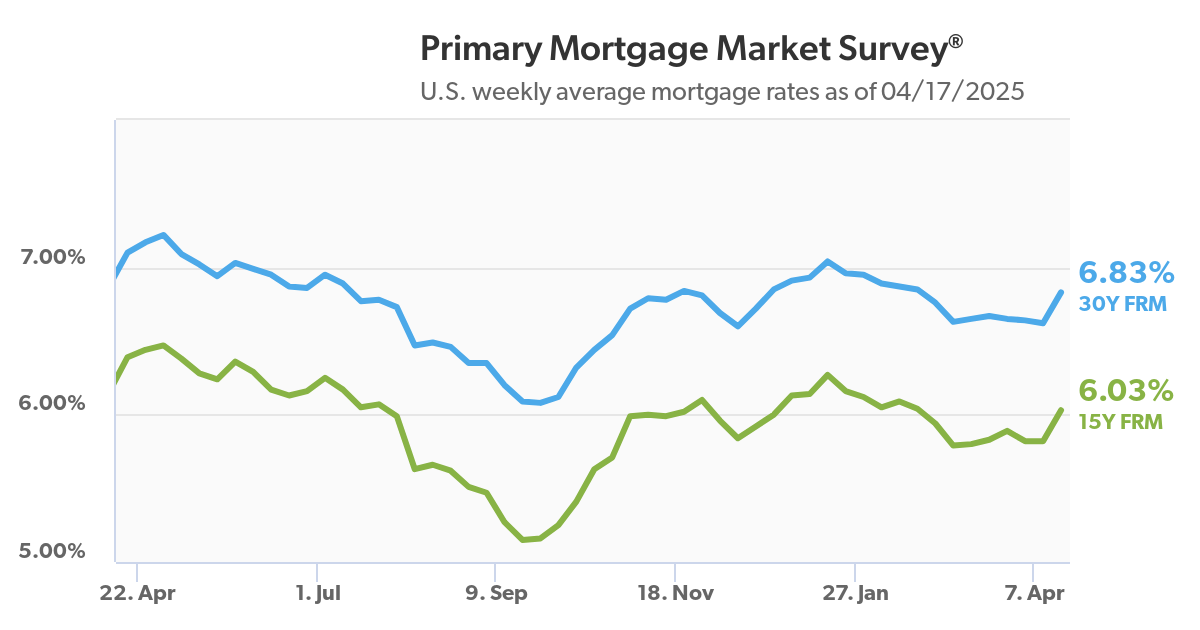

The Silver Lining for Homebuyers in Today's Market

Most would-be homebuyers consider the recent interest rate rises as bad news. However, there's also an unseen benefit, as fall and winter are historically the times of the year when the housing market shifts in favor of buyers.

In addition, home price growth is cooling down compared to the last two years. More good news: inventory is up by 28% year over year, with some sellers lowering their prices and more likely to negotiate with a dwindling pool of buyers.1

Put Safety First When Showing a Property

Real estate can be a potentially dangerous business when an agent meets an unknown potential client at an out-of-the-way place.

Being aware of your surroundings is not enough. Ideally, you'll meet an unknown client with a third party, like a friend or another agent.

Get Pre-Approvals

No matter where the lead came from, you should make sure that the prospect has been pre-approved. Ask for the lender's pre-approval to be sent to you in advance. This helps separate serious homebuyers from potentially risky situations.

Vet Clients

After you have their pre-approval, ask the new client a series of questions to help ensure you know their plans. These may include: "How soon do you need to move in?" and "Are there any other decision-makers involved?"

Prep for a Safe Showing

Safety preparation goes further than the standard prep for showings. For example, always have your mobile phone where it's easily accessible. Also, make sure your clients meet you at the office first, then ask them to follow you in their own car. That way, you can always get away if necessary.2

Negotiation Mistakes to Avoid

A strong negotiation strategy can significantly increase your success as a real estate agent by deepening your relationships and increasing client satisfaction. Keep your reputation safe and your sales high by avoiding these five mistakes:

Mistake #1: Being unprepared

Plan and strategize before you head to the negotiations table. Over-prepare ahead of time to ensure you don't have regrets.

Mistake #2: Becoming intimidating

Stay cool and don't let your negotiations get heated, defensive, or out of control. If you reach the intimidation zone, you'll rarely win and likely won't get a second chance.

Mistake #3: Rushing things

Be patient and stay calm. Waiting out an opponent is one of the strongest advantages in any negotiation.

Mistake #4: Talking a lot

The go-to motto in negotiations is "silence is power." This may cause your opponent to trip up and share something that gives you the advantage.

Mistake #5: Avoiding conflict

Conflicts happen, especially in negotiations. Don't take it personally and let the natural give-and-take guide you to a strong position.3

New Affordability Facts for Homebuyers

After almost three years of a sellers' market, the real estate tide has finally turned in favor of homebuyers. This is highlighted in new findings from the Mortgage Bankers Association that outline the details of the current lending landscape.

Here are three affordability takeaways for homebuyers:

The median loan amount peaked

Down from its highest point of $340,000 in the first quarter of 2022, the median loan amount in August was $313,500.

The median mortgage payment applied for decreased

For the third month in a row, the median monthly payment borrowers applied for decreased. By August, it was down to $1,839.

Don't apply for credit.

When lenders are working to verify a borrower's income, they look at their debt-to-income ratios and pull credit. Tell clients to avoid opening any new lines of credit before closing, as it could increase their mortgage's interest rate – or worse, they may no longer qualify for a loan.

Homebuyer affordability increased

Buyer affordability increased slightly across Black, Hispanic, and White households based on new, lower monthly mortgage payments relative to income.4

A Brief History of the American Mortgage

The history of the American mortgage began almost 300 years ago. Home mortgages started in the late 1700s when the first U.S. commercial bank was formed. Five- and six-year loan terms became the norm in the 1800s, with homebuyers usually required to make a 50% down payment.

Also, buyers were only allowed to repay the interest on their mortgages every month during the entire term, which meant that the loan's entire principal was due at the end of the term.

After 40-50% of mortgages went into default after the Great Depression in the 1920s, President Roosevelt created The New Deal – a series of relief programs that included improvements to the mortgage industry. Homeownership skyrocketed during the 1940s - 1960s, fueled by the Servicemen's Readjustment Act of 1944 that created VA loans for military veterans. Today's mortgage industry offers a variety of loan options, including refinancing and equity-based loans to homeowners.5

Sources: 1realtor.com, 2ypn.realtor, 3realtytimes.com, 4mymortgagemindset.com, 5better.com

Recent Comments