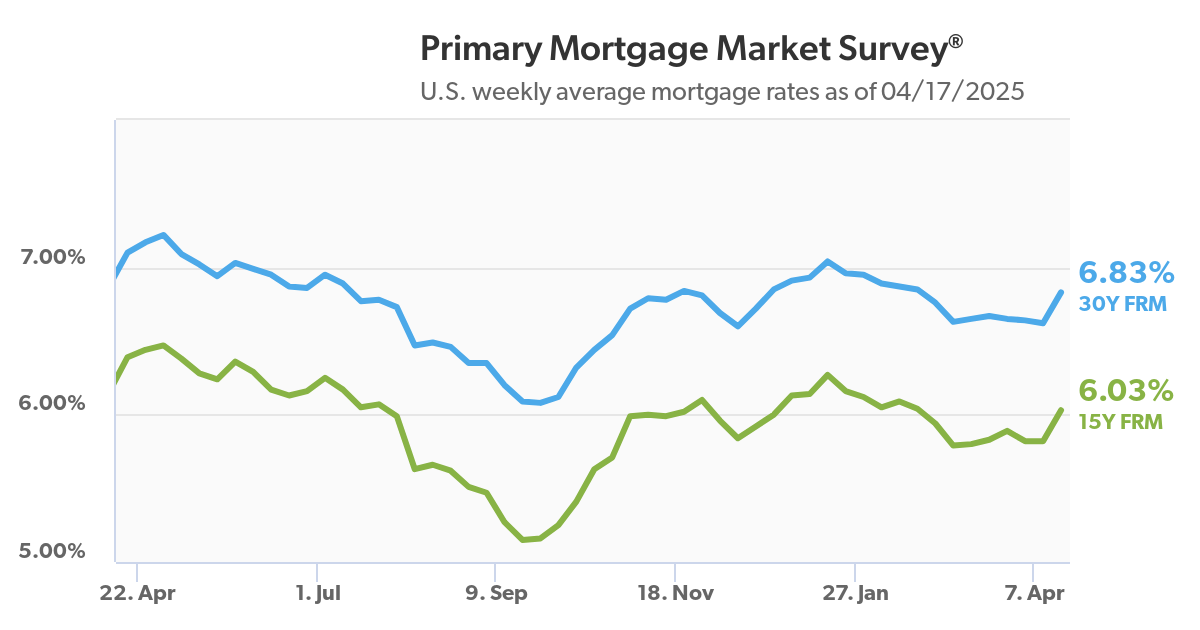

Inflation Numbers Cool in June

Last week, the Consumer Price Index (CPI) declined 0.1% from the previous month, which put the 12-month rate at 3%. This is the lowest CPI level in more than three years and may result in lower interest rates later this year.

While food costs are still high, the core CPI increased by just 0.1% monthly and 3.3% from a year ago. The annual increase for the core rate was the smallest since April 2021.

A 3.8% slide in gasoline prices held back inflation for the month, offsetting 0.2% increases in both food prices and shelter.

Housing-related costs have been one of the most stubborn components of inflation and make up about one-third of the weighting in the CPI. Shelter inflation fell to a 5.2% annual rate, down from around 8% in early 2023 but still above its pre-pandemic baseline.

Economics gurus are feeling hopeful that the Federal Reserve will announce a rate cut during their September meeting, describing the higher CPI numbers during the first quarter of 2024 as a "bump in the road".1

Housing Inventory Heats Up

Monthly data at Realtor.com found that the number of homes for sale rose for the eighth consecutive month, and supply is up 36.7% year-over-year. This means that inventory is higher now than it was during the summers of 2021-2023, and if it continues to grow, it could surpass summer 2020 levels soon.

Some particularly positive news: The supply of relatively affordable homes — those in the $200,000 to $350,000 range — saw the highest rate of annual growth at 50%.

Florida led the way earlier this year in inventory growth, with Tampa supply surging 92.7% and Orlando up by 81.8%. Austin, San Antonio and Memphis are back to pre-pandemic inventory levels, while Nashville is just 1% below the levels seen five years ago. Las Vegas was the only major metro seeing a 29.5% decrease in homes for sale.

Regionally, the South and West are experiencing the highest growth, with inventory rising 48.7% and 36.5% respectively year-over-year. The Midwest (up 21%) is next, followed by the Northeast (11.8%).2

Are Rental Properties Better Than College Dorms?

Even though parents begin saving for their children's education decades in advance, their bank balances may not keep up with rising costs. In addition to tuition, books and living expenses, students who leave home for school will be paying for room and board.

Since college dorms add thousands to tuition bills, some parents buy a second property as an alternative. While this can be a smart decision, you'll want to counsel these buyers by encouraging them to do their homework first. Here's why.

- Some schools require students to live on campus during their freshman year or longer.

- Not all students want the responsibility of living in a place their parents bought. Some may find this overwhelming.

- Buying a larger property and charging other students rent can be time-consuming and potentially risky.

- Is there a possibility that the child will transfer to another college? What would happen to the rental property if this happened?

More Younger Buyers Choosing Fixer-Uppers

While most buyers prefer modernized, move-in-ready homes, some bargain hunters are still willing to buy a fixer-upper. A new survey of around 1,000 Gen Zers in their 20s found that more than half of them were willing to consider an unmodernized home. However, around 27% of the respondents who had already bought one were rethinking their decisions.

Would-be buyers need to keep renovation costs in mind, as well as the home's current functionality. Will they be able to move in after closing, or will they have to wait until after essential plumbing or electrical repairs are completed?

If you're involved in the sale of an unmodernized home, here are areas that need a closer look:

Roofs: Repairs can incur a significant cost, and earlier leaks may have caused more damage than you'll see during a walk-through.

Plumbing: Any pipes installed before 1980 will need special attention, as older materials are more likely to leak.

Electricity: Find out when the home's wiring was last updated. Older homes often lack safety features like ground fault circuit interrupters (GFCIs). The electrical panel, aka breaker box, can also provide clues about the home's safety.

Walls: If you spot cracks in walls, uneven floors and sticking doors, there could be expensive foundation repairs in the buyer's future.

Land: In addition to FEMA flood ratings, look for evidence of flooded basements or erosion. Some types of soil are less stable than others, which means that one heavy rain can cause an expensive, unwanted surprise.4

Be Careful with These Marketing Cliches

1. I'm The Top Agent Here

This claim is frequently used (Google it!) but rarely true, so you'll want to avoid it. This doesn't mean you should avoid mentioning your achievements, as long as you can provide proof. In addition, make sure a claim is meaningful to potential clients, who may or may not know what a "top closing ratio" or similar claim means.

2. I'm Your Neighborhood Specialist

Again, if this isn't true, your market will see right through you. If you have plenty of listings in a desirable neighborhood, this is a start, but you should also be able to discuss schools, tax rates, and other things that potential buyers will want to know.

3. I'm In the Top 1% of Agents

This claim has been abused to the point where it's a major turn-off. Even if you can prove this, it's better to mention this elsewhere, so you can provide details of when and where you were in the top 1%.

4. I Scored the Highest in Customer Satisfaction

Again, this is a cliche that's best avoided in the headline. If you have plenty of five-star Google Reviews or manage your client feedback with a suitable app or web site, you can mention this (with links to your proof) during a new client presentation or within a blog article.5

Sources: 1cnbc.com, 2realestatenews.com, 3lightersideofrealestate.com, 4cnbc.com, 5theamericangenius.com

Recent Comments