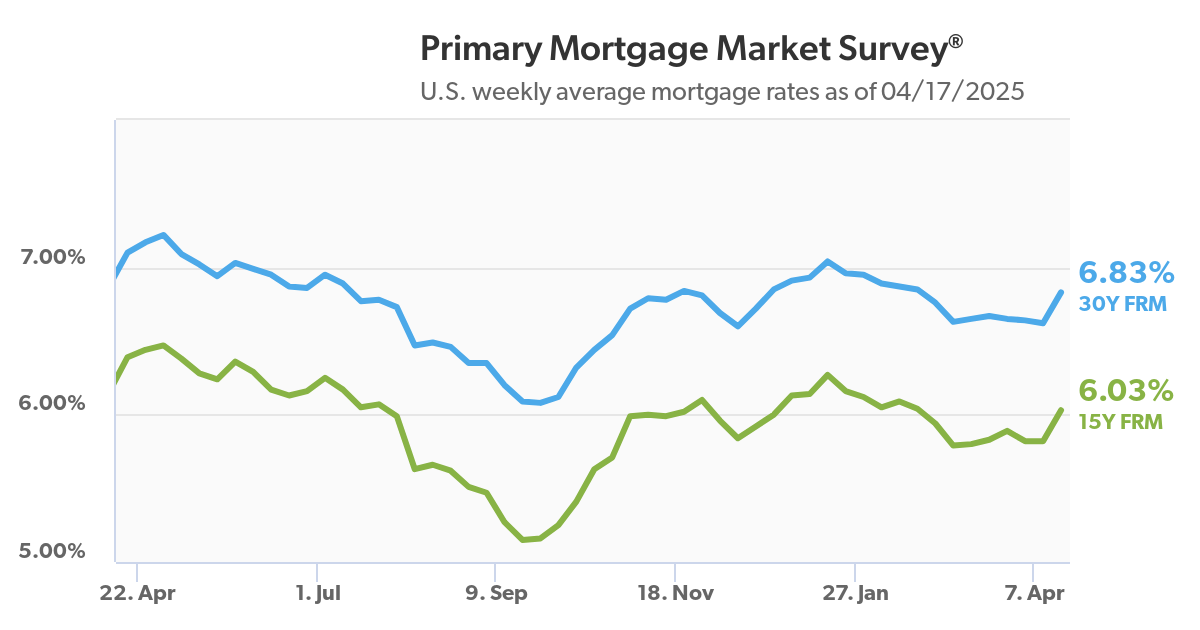

Buyer Purchasing Power Continues to Recover

During the last months, mortgage interest rates have reacted to favorable economic news and are now considerably lower than last October's painfully high numbers. This adds up to additional purchasing power for your buyer clients.

For example, homebuyers on a $3,000 monthly mortgage repayment budget may qualify for financing for a $453,000 home with a 6.7% mortgage rate (depending on down payment, credit score and other factors). This adds up to a nearly $40,000 increase in purchasing power when compared to last October.

For example, homebuyers on a $3,000 monthly mortgage repayment budget may qualify for financing for a $453,000 home with a 6.7% mortgage rate (depending on down payment, credit score and other factors). This adds up to a nearly $40,000 increase in purchasing power when compared to last October.

To look at affordability from another perspective, the monthly mortgage payment on a typical home, with a sticker price around $363,000, is $2,545 with a 6.7% rate. The monthly payment for the same property was nearly $200 higher–$2,713–when rates were at 7.8%.

While today's mortgage rates are still double the record-low pandemic rates, more agents and lenders are reporting that home buyers are coming to terms with mortgage financing that's within the 6% interest rate.

A Seattle-based agent commented: "Now, buyers are snapping up homes because even though rates haven't plummeted, people are realizing that the longer they wait to buy a home, the more competition they're likely to face."1

We Can Help Homebuyers with Disabilities

Did you know that over 10% of our nation's population is classified as legally disabled? Even with often-limited incomes, they may qualify for one or more loan programs, especially federally insured mortgages such as FHA, VA and USDA loans. These loans often accept disability income, as well as Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI). Long-term disability income from an insurer or employer may also help your buyer client qualify.

Like any other form of income, disability income needs to be properly documented for a lender's underwriter to consider it within a loan application. Long-term disability generally needs to continue for at least three years, although proof of a future return to work in less than three years may also be accepted.

If your client is a disabled military veteran, the VA loan program may be an option. In addition to these loans' no down payment requirement, some veterans with disabilities may also have their funding fee waived. Some veterans may also qualify for a property tax exemption and/or a mortgage tax credit.

Buyers with disabilities whose income falls below the area's median income may qualify for a USDA Single Family Housing Direct Loan. This program is subsidized, which means that the USDA will cover a portion of monthly loan payments. Another potential advantage: considerably lower interest rates modified by payment assistance.

Contact me to discuss how we can assist disabled buyers by providing the stability of home ownership.2

Buyers' Strategies for Shopping Limited Listings

If your listings aren't all move-in ready homes, here's some good news. A survey published earlier this month found that 80% of the prospects planning to buy a home this year are less picky than in previous years. Instead, they're willing to buy a property that isn't the traditional, picture-perfect 3/2/2 home.

Here are some takeaways from the survey:

- Buying a fixer-upper has become a popular strategy, with over 50% of survey respondents willing to consider one. (Special "rehab" financing for these properties may be available...ask me for details.)

- Almost all respondents willing to consider a fixer-upper would also consider buying a foreclosed property.

- Around 39% of respondents would consider a prefabricated or even a tiny home.

- More buyers are learning that a 20% down payment isn't mandatory. Over 30% of respondents plan to buy with a smaller down payment.

- Around 28% of would-be homeowners are planning to buy a condo or townhome.

- The same percentage are considering finding one or more co-borrowers to share the costs of a mortgage.

Virtual Staging Dos and Don'ts

Unfurnished, empty listings can be a hard sell, even with today's shortages of homes for sale. This is when virtual staging can be useful. Whether you have the expertise to do this on your own or hire a specialist, here are some things to keep in mind.

Start with high-quality photographs. It's important to know how lighting and shadows will affect the room, and that any special design details are highlighted.

Be ethical about virtual staging. The goal of virtual staging is to show a home at its best, as this will help buyers think about making it their own. Don't use staging to hide flaws in the home's interior. Also, be careful to place televisions and entertainment systems near existing power sources.

Choose furnishings and décor that complement the property's style. Digitally placing sleek, contemporary furniture in a rustic farmhouse can turn off buyers, for example.

Break up boring walls. While it's easy to go overboard with staging, there's also the risk of going to the other extreme. Experiment with various wall decor and framed art.

Don't forget the bathroom. You can't alter the tub or vanity, but you can spruce up a lackluster bathroom with a plant, lamp or a colorful rug.

Tidy up the exterior. Replace dying plants and rusting outdoor furniture with virtual versions.4

Best Practices for Your Social Media

Create a social media policy. These are helpful, whether you're part of a brokerage or an independent. Ideally, your policy should include content and brand guidelines, an approval process and rules regarding sharing other agents' listings. Any state laws that affect you should also be included.

Set up a social media listening process. Monitor your accounts for comments and likes. This helps you stay compliant while providing opportunities to engage with clients who reply to your posts.

Protect your account. Be aware of common social media hacks and scams that affect our industry. Protect your accounts with two-factor identification and solid passwords.

Archive your social media activity. These may be valuable if someone misquotes you, or you want to find an older post about a listing that's just come up for sale. Facebook and other social media platforms have instructions for archiving your activities.

Batch and schedule future posts. Not only does this help you stay focused, but it also saves time and helps prevent repetitive postings. You'll also be able to review what you've created before it goes live or ask a colleague to double-check for accuracy and compliance.5

Sources: 1redfin.com, 2themortgagereports.com, 3dsnews.com, 4snappr.com, 5blog.hootsuite.com

Recent Comments